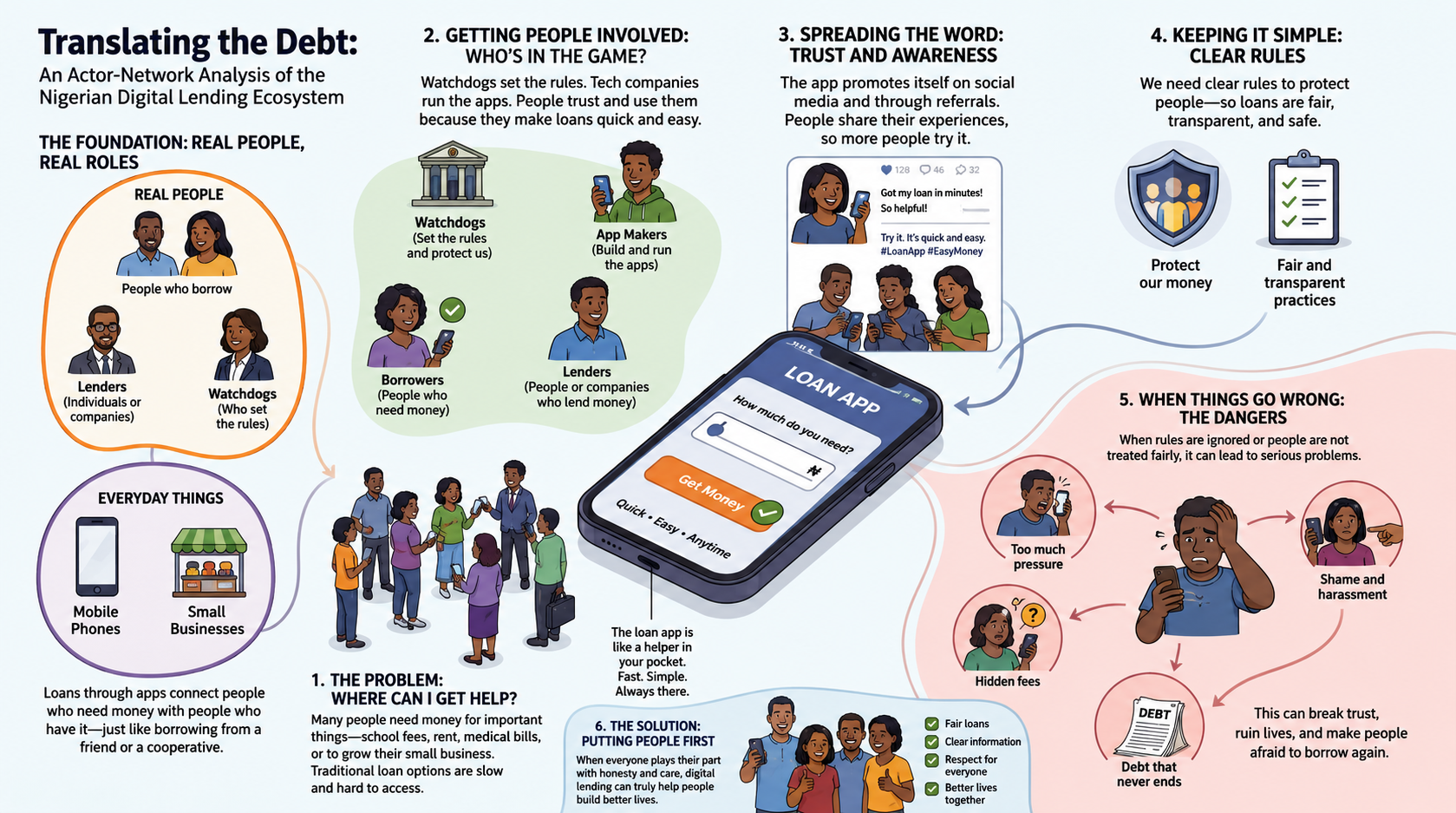

The digital lending crisis in Nigeria is often discussed in simple terms: greedy lenders, desperate borrowers, and regulators trying to catch up. However, if we look more closely at the chaotic world of “loan sharks,” “public shaming,” and “police raids,” it becomes clear that this isn’t just a story about human choices. It is a story about a living system where technology, economic pressure, and physical devices are just as influential as the people using them. To find a real solution, stakeholders must stop viewing the mobile phone as just a tool and start seeing it for what it truly is: the heart of the entire lending ecosystem.

The Smartphone: The Silent Partner

In this lending world, the mobile phone is far more than a communication device. It is the physical glue that holds every relationship together. Without the phone to host the app, the lender and the borrower would never meet. But the phone does more than connect them; it defines who they are to each other.

When a borrower installs a loan app, their identity shifts. They are no longer just a person; they become a data point defined by their contact list, their GPS location, and their photo gallery. The phone acts as an active participant that “does things”—it gathers information, sends aggressive reminders, and, in the case of “unorthodox recovery practices,” provides the very ammunition (contact lists) used for public shaming. The technology and the human user are so intertwined that you cannot influence one without addressing the other.

The Struggle to Set the Rules

For regulators like the FCCPC and the Central Bank of Nigeria, the challenge is one of alignment. They are trying to create a system where every player is forced to follow a specific path. We see this in their strategic partnership with Google to enforce “Play Store Policies”.

By doing this, regulators aren’t just writing laws; they are trying to recruit a powerful technological ally to do the policing for them. If Google blocks an app, the lender’s network vanishes. This is a sophisticated game of negotiation where the government tries to “lock in” technology companies to ensure the system remains stable and safe for consumers.

When the System Breaks: Defaults and Betrayals

The reason this ecosystem feels so volatile is that it is incredibly fragile. Every connection in the network depends on everyone—and everything—staying in their assigned place. When a borrower “defaults” on a loan, they are doing more than just missing a payment; they are refusing to play their part, causing the lender’s entire business model to shake. In a desperate attempt to force the borrower back into the system, lenders resort to “Public Shaming.” This isn’t just bad behaviour; it is a mechanical reaction by a system trying to repair a broken link. However, these aggressive tactics often backfire, leading to “Police Raids” and a complete breakdown of trust, proving that a system built on threats is inherently unstable.

The Power of a Unified Voice

One of the most significant shifts in this landscape has been the rise of the “Mobile Loan Apps Debt Victims” Facebook page. In the past, victims were isolated and powerless. Today, this social media platform acts as a representative for thousands of individuals. It takes scattered, private experiences of abuse and transforms them into a single, public grievance that regulators cannot ignore. It has created a counterforce that challenges the lenders’ power. This reminds us that power in the lending world isn’t something one person “owns”—it is a result of how well you can keep your supporters and your technology working together toward a common goal.

A Way Forward for Stakeholders

Regulators: The message is that you cannot just regulate human intent. You must regulate the physical links, the data flows, the app permissions, and the digital platforms that hold these relationships in place.

Digital Lenders: The lesson is that a business built on “unorthodox practices” is a house of cards. When the technology (like Google’s algorithms) or the collective voice of the victims shifts, your entire network can disappear overnight.

The Nigerian digital lending market is a complex web of people and machines. Only by recognising that the “non-human” parts of this web, the phones, the apps, and the data, are just as active as the “human” parts can we hope to build a financial system that is durable, ethical, and truly serves the public.

Leave a Reply